Everyone needs cash at least occasionally. In some places and situations, it is the only way to pay. The recipient might be unable to accept non-cash payments, or the payer might not have access to other payment methods. And sometimes, people simply prefer to use cash. Ultimately, the choice of payment method is up to the individual.

The use of euros is not confined to eurozone countries. In the highly digitalised Nordic countries, for example, euro cash can in places be used alongside crowns. There are also regions outside of Europe where euro cash is accepted alongside the local currency.

In 2023, the European Commission adopted a legislative proposal on the legal tender of euro banknotes and coins. The proposal is currently under discussion in the Council and the Parliament. The Commission, the Council and the Parliament have worked commendably during the drafting process to ensure that euro cash remains a payment method in the future.

Challenges related to physical cash have also been identified in the process.

Cash is losing ground to other increasingly more digitalised payment methods and instruments. Future payment systems rely on fewer mechanical solutions, as visible infrastructure becomes ones and zeros. Digitalisation makes payments safer and more streamlined, but cash will still retain its own uses.

======

What will happen to cash after the digital euro?

======

Plans to introduce a digital version of cash in the eurozone are moving forward. The same Single Currency Package that includes the regulation on the legal tender of euro cash also includes a proposal for a digital euro. The purpose of the digital euro is not to replace cash but to complement it. It is quite possible we will see the new payment instrument in action before the end of the decade. The declining use of cash is pushing up the costs, making it more and more difficult to organise cash services using a market-based approach. The fates of both euro cash and the digital euro depend on their respective costs, pricing and compensation models.

The ongoing cash debate has mainly focused on consumers and the availability and usage of cash. The majority of cash enters circulation through ATMs. It is the preferred payment instrument especially among young people, which can be attributed to the age restrictions on digital services.

The question of how cash is distributed in the first place has received less attention. In this area of cash infrastructure, national central banks play a key role.

In Finland, cash is issued by the Bank of Finland: it orders euro cash from the European Central Bank and distributes it to the Finnish market. The physical delivery of coins and banknotes to commercial banks, businesses and ATMs is carried out by cash management and cash-in-transit companies. The companies also collect cash from banks, businesses, deposit machines and night depositories and deliver it to private cash centres to be counted.

As the world turns and changes, the national central bank’s role has adapted. The Bank of Finland has reduced the number of its own cash centres to one and implemented a Notes Held To Order (NHTO) system to ensure the cash infrastructure remains functional. Because all the other cash centres are now managed by private parties, the Bank of Finland no longer handles primary cash transport between the centres.

How cash transport between the Bank of Finland and the end-users of cash is arranged and managed is by no means an irrelevant detail. If market-based operations become unprofitable, the next step in the cash debate is to launch a comprehensive reassessment of the cash infrastructure and consider possible compensation models.

As for now, cash is still in demand and in widespread use. Whether it remains a viable payment instrument in the future will depend on the deeper structures of the cash infrastructure.

Still have questions?

|Contact the columnist

Looking for more?

Other articles on the topic

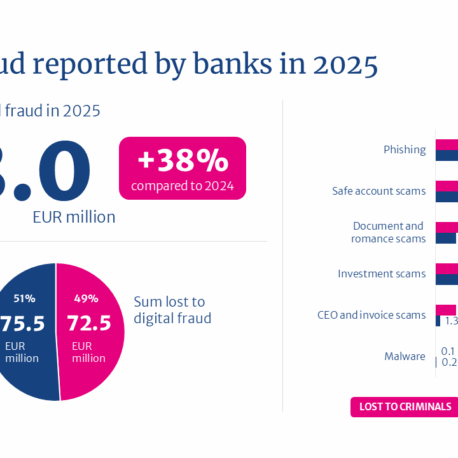

Total value of attempted digital fraud climbed to €148 million in 2025, but banks successfully intercepted more than half of the payments

Even a prolonged service disruption will not stop in-store payments – Finance Finland publishes report on the resilience of card-based payments

Cash is about more than just ATMs and shops – how can we secure Finland’s cash supply?

FIN-FSA surveyed financial sector companies’ use of AI – from crunching data to fighting financial crime