- Each party in the card payment process must be prepared for service disruptions to ensure the continuity of its own operations.

- If the operations of one party are disrupted, this can halt the entire process chain unless the disrupted party has adequately prepared for the scenario.

- It is possible to enable offline payment on a payment terminal if the terminal is disconnected from the authorisation network despite preparedness measures.

- The continuity of card payments must be safeguarded using a market-driven approach rather than through regulatory means.

- National legislation can only impact a limited number of actors on a local level. However, parts of the payment process chain may be located abroad.

- Changing the rules and guidelines of international card schemes is a swifter and more effective solution than regulatory steering.

Finance Finland conducted an assessment on the resilience of card-based payments during prolonged payment service disruptions. The assessment report presents a situational picture of in-store card payments in Finland, recommendations for disruption preparedness and an overview of existing solutions that enable payment continuity during a prolonged disruption.

Each party in the card payment process must independently prepare for disruptions within its respective responsibilities. Securing real-time information exchange is key to ensuring payment continuity. The successful transmission of a card transaction from the payer to the merchant relies on all links in the payment chain.

“If disruption preparedness is inadequate, a failure in one link in the chain can interrupt the entire transaction. Parties commonly involved in the card payment process include, for example, card schemes, merchant payment service providers, merchants and card issuers”, says Kirsi Klepp, author of the assessment and head of card payments infrastructure at Finance Finland.

Incidents that disrupt card payments are rare. However, each party involved in the card payment chain must independently implement backup systems. This way, payments can continue even during disruptions as long as there is adequate power supply and functioning telecommunications connections.

“Even if the payment terminal is disconnected from the authorisation network, card payments will function as usual from the customer’s perspective. The merchant stores transactions locally in a buffer and obtains authorisation from the issuer once the connection is restored. The key message of the assessment is that all disruption preparedness measures must aim to ensure that payments can continue in a manner that is as close to normal as possible.”

“The aim of disruption preparedness is to ensure that payments can continue in a manner that is as close to normal as possible.”

KIRSI KLEPP, Head of Card Payments Infrastructure

Market-driven development and flexible legislation

In Finland, the operational reliability of card payments has been developed primarily on a market-driven basis, and cooperation between public authorities and market players has been transparent and efficient.

Amending legislation is a slow process, and steering the market through legislation is challenging. Due to the international nature of card payment services, local legislation can only impact a limited number of actors.

International card schemes play a decisive role in card payments – their rules and guidelines enable swift and uniform implementation across the entire card payment chain and support the continuity of card-based payments in Europe.

“The development of payment services should be continued with a market-driven approach and through legislation that allows flexibility in diverse types of payment situations. Customers prefer to continue using their usual payment methods also during disruptions. In all circumstances, the ultimate choice of payment method is made by the consumer”, Klepp concludes.

Still have questions?

|Contact our experts

Looking for more?

Other articles on the topic

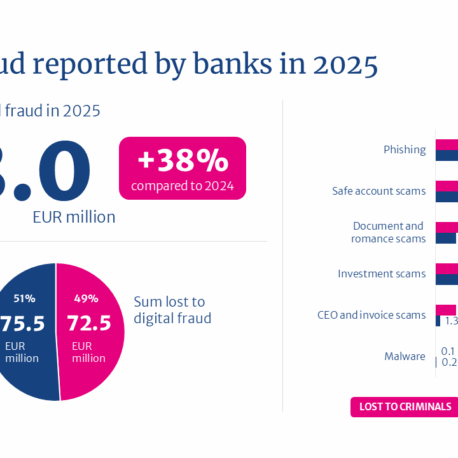

Total value of attempted digital fraud climbed to €148 million in 2025, but banks successfully intercepted more than half of the payments

Even a prolonged service disruption will not stop in-store payments – Finance Finland publishes report on the resilience of card-based payments

Cash is about more than just ATMs and shops – how can we secure Finland’s cash supply?

FIN-FSA surveyed financial sector companies’ use of AI – from crunching data to fighting financial crime