Less is more – EU regulation must not become an end in itself

- Not all problems can be solved through new regulation. Often it is enough to clarify existing rules, improve implementation and develop supervision.

- Promoting growth and competitiveness must be set as one of the guiding principles when new regulation is being considered.

European financial sector regulation has expanded and become increasingly complex, which weakens the sector’s competitiveness and increases the administrative burden.

The current geopolitical and geoeconomic operating environment hinders Europe’s competitiveness and security. Breaking the cycle of slow growth and low productivity is essential. Regulation must support growth, and we therefore call for targeted recalibration of regulation.

The primary measures should be regulatory streamlining and precise reviews of core rules. The objective must be improving business conditions and reducing the fragmentation of EU capital markets.

1

Simplification and the principles of better regulation

- The European regulatory framework has expanded and become increasingly complex, which weakens competitiveness and increases administrative burden. Not all problems can be solved through new regulation. Often it is enough to clarify existing rules, improve implementation and develop supervision.

- We consider it extremely important that new regulation is not treated as the primary solution if the same objectives can be achieved through lighter means, such as the clarification of existing regulation.

- Completely new regulation must be based on comprehensive impact assessment. The impact assessment must clearly define the problem being addressed and analyse the effect of the proposed measures.

- We consider it important that the Commission continues the simplification of the current framework of financial sector regulation. This work should focus on the elements that deliver genuine added value, consistency and clarity. Removing irrelevant details or merely postponing the regulation may increase uncertainty or lead to very costly changes to IT systems. The Commission should develop a strategy for identifying the key legislative texts that cause the greatest administrative burden and uncertainty.

2

Multiple levels of regulation increase complexity – but reviews must be performed with caution

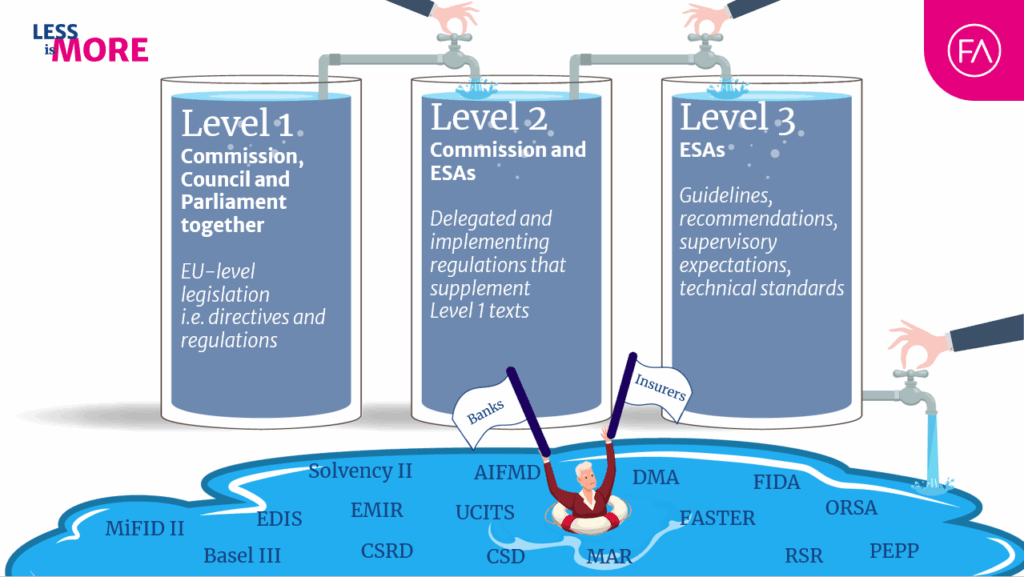

- Financial sector EU regulation is typically depicted as three-tiered, as illustrated above. As each level adds to the previous, the outcome is a sea of regulation in which sector participants try to stay afloat as best they can.

- The aim should be to permanently reduce the amount of key texts on level 2, as they are one of the main reasons for the significant increase in regulatory obligations.

- In general, reviewing EU regulation is justified only when there is genuine need. Clear criteria must be defined and met before initiating the review process. Continuous regulatory reviews almost always result in changes that must be implemented, which causes a significant drain on resources that companies could otherwise invest in innovation and development.

3

Supervisory mandates should incorporate competitiveness

- The mandate of national and European financial supervisors must be balanced so that competitiveness and economic growth are integrated as complementary goals alongside stability and investor protection. National supervisors can enhance competitiveness by utilising macroprudential tools and issuing recommendations and binding decisions. European supervisors can enhance the attractiveness and efficiency of EU financial markets through lower-level regulation and supervisory guidelines.

- At the same time, it is vital to preserve the priority of the primary mandate – safeguarding financial stability. Financial stability must be secured before competitiveness is promoted. Competitiveness should also be incorporated in impact assessments as a central element.

4

Clear limits to the scope of financial supervisors’ powers

- Political decision-making must not be shifted to supervisory authorities. The scope of the ECB’s regulatory powers should be brought up for discussion at the national and EU level. The non-binding recommendations and soft law instruments issued by supervisors must not turn into de facto binding requirements.

- The powers to draft detailed rules that is conferred on financial supervisors by regulation must be clearly defined.

Contact our experts

-

Mari Pekonen-Ranta

Director, EU Affairs

Director of the EU Affairs team, Member of the Management Team, Secretary of the Board, coordination of EU lobbying, Brussels office

-

Miikkael Azaize

Head of EU Affairs, Brussels

EU lobbying, Brussels office