Banks’ risk reduction is a prerequisite for a common deposit insurance scheme

- Finance Finland supports the idea of deposit insurance and deposit guarantee funds, but the scheme must be designed so that compensations are available at need and distributed fairly.

- Until risk reduction in the Banking Union is complete, the current model based on national deposit insurance schemes is a good option for Finland.

- Arguments in favour of EDIS often bring up depositor protection and prevention of contagion risk. However, when national deposit guarantee schemes are taken into account when examining the solvency and crisis management frameworks, depositor protection is already in place.

- Banking does not take place in a void. Banks need to raise the necessary funds to pay their guarantee fund contributions. In the corporate world, there are two ways to do this: improving efficiency or increasing revenue. The payments into a common deposit insurance scheme thus directly influence banks’ operations also competitively speaking.

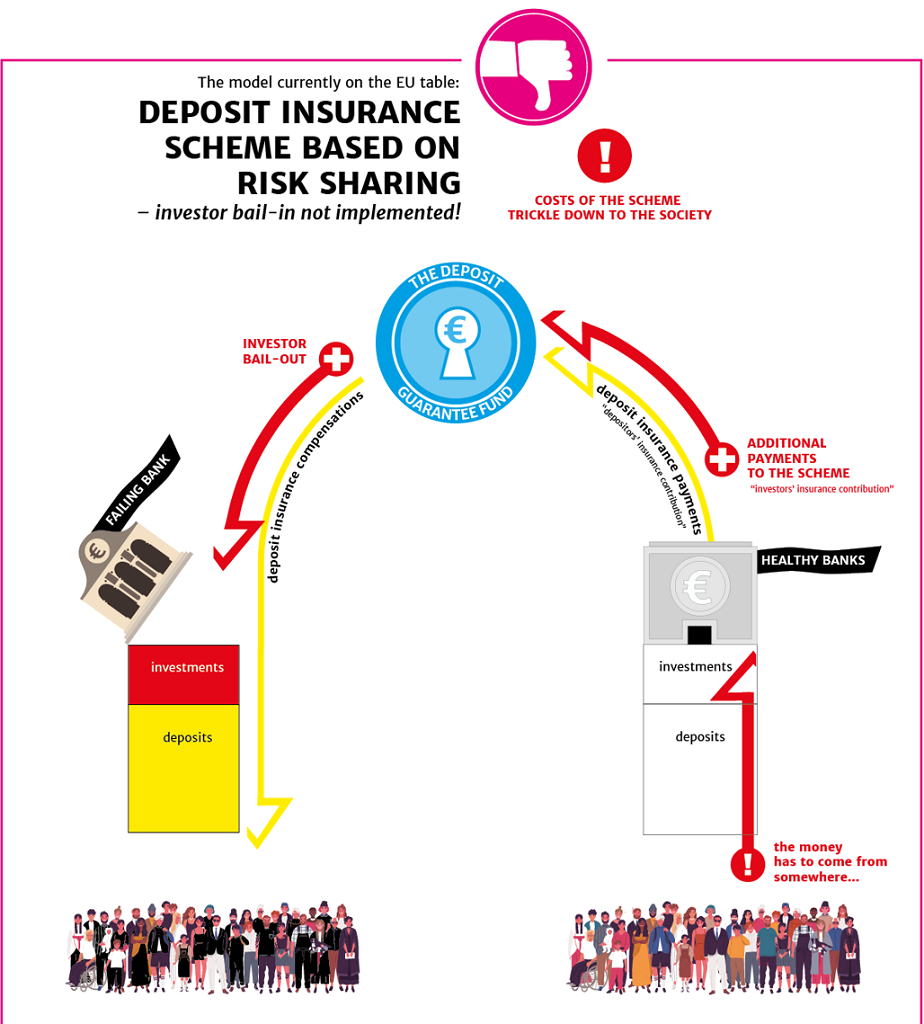

An unfair model would be based on risk sharing

An unfair deposit insurance scheme would also cover investor losses. If a bank then runs into problems, the scheme’s assets would be used for purposes that may benefit the bank’s owners and other investors instead of its actual purpose, which is to protect the bank’s depositors. These funds may be unrecoverable. Drawing on the scheme’s assets will drain them and make it necessary to raise deposit insurance contributions. This will increase costs for other member banks and may negatively impact their lending, for example. Thus, costs resulting from losses would be pushed to external parties instead of banks’ investors.

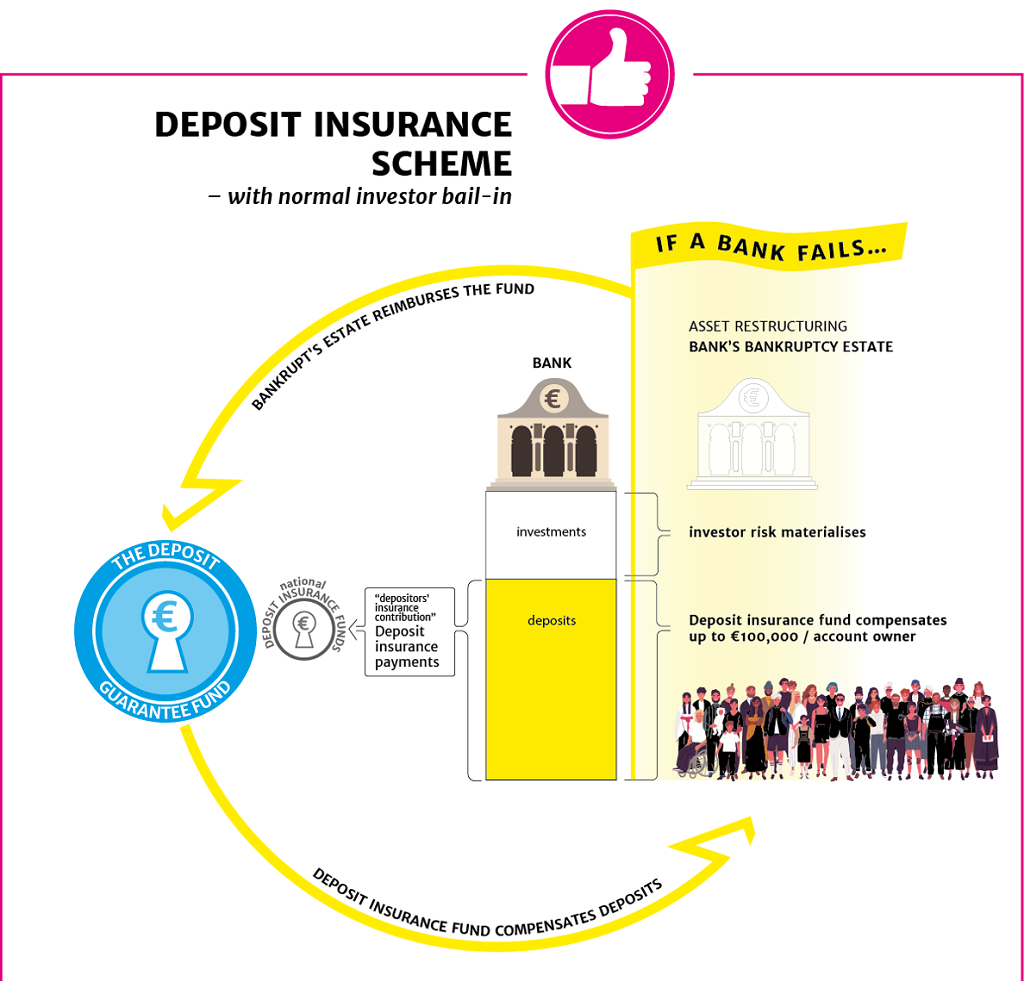

A fair model has normal investor bail-in

In a fair scheme, each bank pays contributions to the fund for the eventuality that it becomes unable to pay back deposits. If the bank fails, its depositors will be compensated by the bank or, if the bank is insolvent, by the resolution fund for up to €100,000. The resolution fund will be fully compensated by the bank’s estate. The bank’s owners and other investors will bear the costs through bankruptcy. The risk that materialises is normal investment risk.

Contact our experts

-

Olli Salmi

Head of Banking Regulation

Basel III, bank solvency and macroprudential tools, bank and insurance company resolution, macroprudence, mortgage banks