- The European Commission proposes that the sending and receiving of instant payments would be obligatory to all banks who already offer credit transfers in euro.

- Finance Finland fully supports instant payments as a valuable service but thinks the transitional periods need to be longer.

- The transitional period after which receiving euro instant payments is obligatory will be six months for euro area member states and 30 months for non-euro area countries. In outgoing payments, the transitional period is 12 months for euro area member states and 36 months for non-euro area countries.

- The proposal is based on the Commission’s dissatisfaction with the slow rate of the euro instant payments’ rollout.

- SEPA instant credit transfers would be available to all citizens and businesses. Instant payments allow people to transfer funds from one EU or EEA account to another within ten seconds at any time of any day regardless of the bank or home country of the payer and payee.

Traditional credit transfers are received by payment service providers only during business hours and may arrive at the payee’s account only by the following business day. Instant payments are highly convenient for family finances and splitting bills between friends, but also in commerce, because they enable the retailer to receive real-time information on the payment. The service will continue to improve as more and more businesses make use of these real-time payments.

“Finnish banks already receive instant payments on payee accounts, but the readiness to send instant payments varies between individual banks”, comments Finance Finland’s Head of Payment Systems Inkeri Tolvanen.

The Commission proposal aims to remove the barriers that prevent instant payments and their benefits from becoming more widespread. According to the Commission, the universal availability of instant payments is a necessary part of updating and modernising the Single Euro Payments Area (SEPA). Instant payments will enable banks and fintech companies to develop new payment solutions, especially at the point of interaction (for example, a payment terminal or e-commerce).

Timetable puts pressure on banks

The Commission proposal has very strict implementation deadlines. The transitional period for the receival of instant payments is six months and for the sending euro instant payments and for the name and payment account verification service only 12 months.

“Instant payments offer a wide range of benefits to the society, but banks should be given enough time to implement the necessary changes. Many of them are significant, and yet according to the Commission proposal they must be carried out within a year”, points out Tolvanen.

In some countries, it has been more expensive for the customer to send a SEPA instant credit transfer than a traditional credit transfer. This price difference would no longer be allowed.

The security of instant payments would be improved by requiring all providers of instant payments to verify that the account number and the name of the payee match. This way the payer could be warned about possible errors or fraud attempts before the payment is authorised.

Payment service providers are under the obligation to prevent payment transmission to persons and companies on the EU sanctions list. This is currently carried out on a transaction-by-transaction basis. If the payment service provider has not been able to complete the screening process in the maximum execution time for instant credit transfers, the sanction screening of payment transactions leads to a rejection of the instant payment. To prevent unnecessary rejections, the proposal would have payment service providers shift from screening payment transactions to screening their payment service users against the EU sanction lists at least once per day and every time the lists are updated.

Looking for more?

Other articles on the topic

Digital euros must be phased in gradually – starting issuance with a big bang would place considerable burden on all stakeholders

Only a few charges away from anarchy

“AI requires clear rules, but vague and rushed regulation will stall when it matters most”

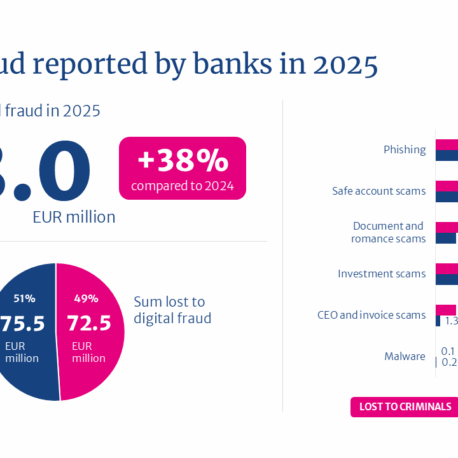

Total value of attempted digital fraud climbed to €148 million in 2025, but banks successfully intercepted more than half of the payments