- The European Commission’s legislative proposal for a framework for financial data access (FIDA), also known as the Open Finance framework, aims to enable customer data sharing and third-party access in the financial sector.

- According to the Commission, the regulation would allow service providers to use customer data to provide new and individually tailored products and services.

- Finance Finland does not believe that the regulation would automatically lead to the creation of new services.

- The costs of the regulation could outweigh its benefits.

- Finance Finland has reservations about the proposal because of its failure to provide concrete and applicable solutions.

- Especially problematic are the definition and categories of customer data.

- As positive elements in the proposal, Finance Finland welcomes the possibility to receive compensation from shared data and supports the fact that data sharing under the financial data access framework is limited to licensed and registered entities only.

- Finance Finland is in favour of a gradual implementation of the framework and at least a three-year transition period for establishing data sharing systems.

The European Commission’s Open Finance proposal is aimed at increasing competition and innovation. The Commission published its legislative proposal for a regulation on a framework for financial data access (FIDA), dubbed the Open Finance proposal, in June 2023. Finance Finland appreciates the proposal’s objectives but fails to see how the framework would automatically give rise to new products, services and innovations. The proposal is also riddled with problems: the regulatory text must be changed to guarantee data protection for consumers and to protect the trade secrets and business models of market participants.

Especially the definition and categories of customer data must be specified in more detail.

“As it stands now, the Commission’s proposal does not adequately account for the data protection and data security of consumers. To achieve this protection adequately, the regulation should define what ‘financial information services’ can be and determine how financial information service providers can use the data they receive. Financial information service provider licences and financial information services under FIDA cannot serve as an express lane to traditional financial sector operating licences. If new service providers want to offer traditional financial sector services, they must meet the qualifications and operating licence criteria required by regulation”, Finance Finland’s Legal Adviser Tuulia Karvinen points out.

According to Karvinen, the proposal’s biggest problem is its lack of concrete solutions. The proposal leaves open a significant number of important matters that should be defined at the level of primary regulation, not secondary regulation.

Finance Finland is in favour of a gradual implementation of the framework and supports the Finnish Government’s position of setting a realistic transition period for establishing the schemes for data sharing. In Finance Finland’s opinion, a realistic transition period would be at least 36 months, preferably longer.

Better-quality service

The Commission is hoping the Open Finance proposal will enable the data-driven development of financial and insurance products, improve the quality of advice given to customers, enhance customer access to services and boost business between companies. Finance Finland fails to see how the regulation itself would directly result in a marked increase in competition and an exponential growth in innovation, as the Commission expects it would.

The Commission’s estimates of the costs of implementing the framework are also unrealistic. Based on the implementation of the Payment Services Directive, the expenses of implementing the Open Finance framework would be considerably higher than the estimate. This is particularly concerning considering that there are no guarantees that the benefits will actually outweigh the costs.

Despite its problems, the proposal also contains positive elements.

“It is good that the possibility to receive compensation from shared data is in line with the recently approved Data Act and that data sharing is limited to licensed and registered entities only”, says Karvinen.

Access to extensive customer data could in theory facilitate the work of financial sector companies and promote a broader range of products and services offered to customers. With more customer data to use, service providers could potentially offer customers more personalised services, tailored to meet their individual needs. But this can only be achieved if the regulation is implemented successfully.

Looking for more?

Other articles on the topic

Digital euros must be phased in gradually – starting issuance with a big bang would place considerable burden on all stakeholders

Only a few charges away from anarchy

“AI requires clear rules, but vague and rushed regulation will stall when it matters most”

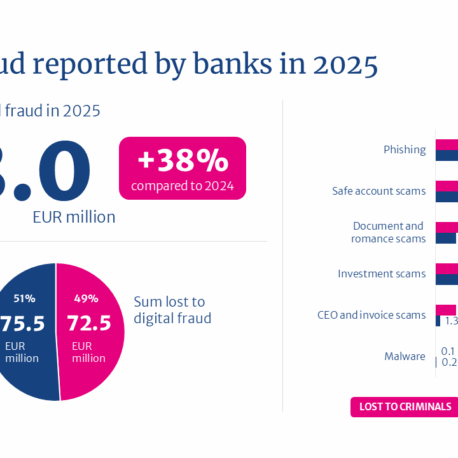

Total value of attempted digital fraud climbed to €148 million in 2025, but banks successfully intercepted more than half of the payments