- The European Central Bank (ECB) is planning to launch a digital euro: a central bank digital currency that would complement coins and banknotes as a payment method. In October, the ECB’s Governing Council decided to move the project to the preparation phase.

- The European Commission has put forward a legislative proposal on the establishment of the digital euro, which is currently being processed by the European Parliament.

- In Finance Finland’s opinion, the digital euro still involves too many unanswered questions and actual risks.

Earlier in December, Finance Finland called together a small roundtable to discuss the digital euro. A full recording of the webinar is available in Finnish at the end of this article.

“I am very concerned about the European Central Bank’s role in the digital euro project. I am fully aware that the global payments industry is controlled by US card issuers – Visa, Mastercard and Amex – and that if their payment transmission gets cut off, it will leave us in a very difficult situation. I understand this security policy aspect very well. But now the supervisor of credit institutions is looking to mess with the market by building a new payment system. This should be seriously questioned”, said the National Coalition Party’s Member of Parliament Aura Salla.

Salla’s concerns are related to the ECB’s dual role: the central bank is currently the supervisor of commercial banks, but the digital euro would also make it also their competitor in payment systems.

Salla is a member of the Finnish Parliament’s Grand Committee, which is debating Finland’s national position on the digital euro initiative. She has demonstrable experience and expertise to take part in the debate: before becoming a Member of the Parliament, Salla worked as public policy director and head of EU affairs for Facebook’s parent company Meta. Facebook was also working on the development of its own digital payment method, Libra, but has since buried the project.

The reliability of payments has become a pressing priority partially due to Russia’s war of aggression and partially due to the political situation in the US. Western sanctions against Russia hinder international payments to and from Russia. In the US, the possibility of another term of Donald Trump’s unpredictable administration has put Europe on edge also in terms of payments.

“Finland has now taken a cautiously positive stance on the matter [of the digital euro]. But we still need more answers to how the digital euro can be made to work in practice”, noted Salla.

Who will cover the costs ‒ and what will happen to financial stability?

Finance Finland’s CEO Arno Ahosniemi understands the European arguments regarding the strategic autonomy of payments. He nevertheless raises three points of concern:

“Financial stability, availability of lending, and costs. For example, if everyone reacts to a deposit run by converting as much of their deposits to digital euros as possible, this will only impair the situation and weaken financial stability. The digital euro would also affect the availability of lending because deposits are a vital and inexpensive source of funding to smaller banks, and if the volume of deposits decreased with their large-scale conversion to digital euros, this would directly impact the lending capacity of small banks. And then there’s the question of costs ‒ which, in a project of this scale, are massive”, Ahosniemi says.

The drafts for the digital euro have posited that an individual citizen could only hold a limited amount of digital euros. Different-sized limits have been tossed around, one of the examples being €3,000. This is approximately the value of euro banknotes currently in circulation divided by the population of Europe.

“The size of the digital euro wallet is a hard nut to crack. If an individual citizen can only hold a few thousand digital euros in their wallet, the currency cannot be used for any major purchases. This will reduce the popularity and usability of the digital euro. But if the limit is very high, it will affect the financial stability of small banks”, ponders Danske Bank’s Senior Infrastructure Manager and Chair of Finance Finland’s Payments Committee Jarmo Heilakka.

Giving credit institutions an obligation to distribute the digital euro without offering them information about how much costs the distribution will generate and how the costs will be compensated is a problem. In the worst case, every payment made with digital euros causes a downright loss to the bank, and the incentives to distribute the new payment method are non-existent.

Head of the Payment Systems Department at the Bank of Finland Päivi Heikkinen sought to alleviate the misgivings, reminding everyone that the project is still in the study phase. The decision to launch the digital euro has not been made yet.

“The central bank moves slowly in such matters. It has been researching this for years and will continue to do so. I can understand the concerns but what we now need is patience. This kind of work cannot be abandoned halfway. If the decision to launch a new payment method is made, it is way too late to be starting a six- to eight-year assessment”, says Heikkinen.

Still have questions?

|Contact our experts

Looking for more?

Other articles on the topic

Digital euros must be phased in gradually – starting issuance with a big bang would place considerable burden on all stakeholders

Only a few charges away from anarchy

“AI requires clear rules, but vague and rushed regulation will stall when it matters most”

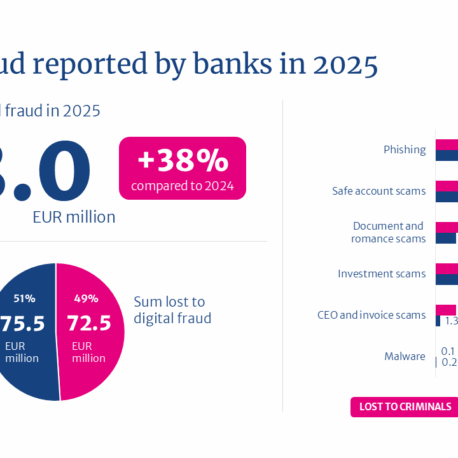

Total value of attempted digital fraud climbed to €148 million in 2025, but banks successfully intercepted more than half of the payments