- Finance Finland has published a report titled “Non-life insurance and climate change”.

- The insurance sector has a vital role in climate change mitigation and adaptation.

- The extreme weather events caused by climate change make risk management and new practices necessary.

- As risk experts and investors, insurance companies have a leading role in building a carbon-neutral society.

The study “Non-life insurance and climate change” was conducted to gather in-depth information on the role of non-life insurance in climate change mitigation and adaptation for the use of FFI and its members. An abstract of the study is available at the end of this article.

Non-life insurance needs a predictable and balanced market and a stable society to function in. Uncontrolled climate change equals an uninsurable world. Climate change affects all industries and functions of society, but the insurance sector plays a key role in the solutions for climate change mitigation and adaptation.

“The insurance sector builds financial resilience against extreme conditions and physical risks by providing risk information, risk pricing expertise, innovative risk transfer products, and knowledge of damage prevention”, says FFI’s Deputy Managing Director Esko Kivisaari.

Risks and damages are related especially to extreme weather events and their frequency, which means the changing climate requires risk management and new operating policies from companies. Although not all climate-related phenomena and damages are in the scope of traditional non-life insurance, it is an essential product for compensating losses incurred from sudden and exceptional events. It is increasingly important for climate change mitigation and adaptation to be part of the regular operations of every company.

According to Kivisaari, the insurance sector has regarded climate change as a major risk already since the 1980s. The rest of the Finnish financial sector has since joined in the fight.

The insurance sector is one of the biggest global industries with insurance premiums of more than 6 trillion dollars and assets valued at 36 trillion dollars. Insurance companies are in a leading position as risk experts, insurers and investors to build and speed up the necessary changes to make the transition towards a sustainable, carbon neutral society.

The insurance sector supports this transition through its insurance activities, investment strategies and the active reduction of its own carbon footprint. The sector itself is not a significant source of emissions, nor is it in a position to lay down climate policies, but it is in a key role in building the society’s socio-economic resilience and steering economic development towards climate goals.

“It is difficult to price physical climate risks because the data on vulnerabilities and exposures is inadequate in many areas. We therefore need close cooperation between the insurance sector and other stakeholders to set down goals and operating models for mitigating climate risks”, Kivisaari states.

One of the tools insurers have is investing. The influential sustainable finance reforms currently being prepared in the EU will facilitate sustainable investment and are relevant for the sector also because they have effects on risk management and customer awareness.

Carbon handprint reveals positive impact

Measuring carbon footprints has become a popular standard of identifying and reducing the negative climate impact of any activity. Reducing the footprint is not enough on its own – we also need to increase positive impacts. This has contributed to the growing demand in carbon “handprints” as a tool to identify, measure and indicate positive impact.

“To assess the handprint of an activity, we need to form a picture of the alternate outcome: what would happen without the activity in question? The handprint of non-life insurance represents the positive climate impact that would not take place without non-life insurance”, explains Elina Levula, CEO of Positive Impact.

According to Levula, non-life insurance products and services have considerable handprint potential. They can be developed in a direction that reduces risks and emissions, promotes sustainable development, and encourages better risk management. Sustainability aspects and carbon neutrality can also be linked to repairs and compensations as well as rebuilding.

The Board of FFI ruled in 2017 that the Finnish financial sector endorses the goals of the Paris Climate Agreement to limit global warming. The sector has signed a sustainable development commitment on its climate goals and monitors the progress of the commitment regularly. The society’s commitments to sustainable development are Finland’s way of implementing the UN Agenda 2030.

Looking for more?

Other articles on the topic

Reputation survey: Public trust in the financial sector has strengthened, driven by transparency and responsibility

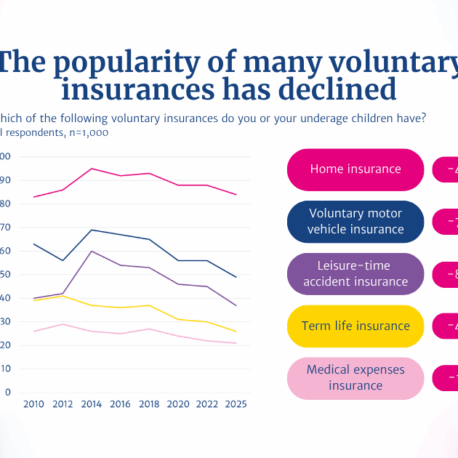

2025 Insurance Survey: Finns have fewer voluntary insurance policies than before

Walking the talk – How financial sector companies are acting on biodiversity loss

Finns are happy with their insurances – 86% consider compensations proportionate to the suffered loss, and claims are rarely rejected